Futures Market: Overnight, LME copper opened at $9,531.5/mt, initially fluctuating upward to a high of $9,574/mt during the session, then fluctuating downward throughout the day. It hit a low of $9,488/mt before slightly rebounding and finally closed at $9,493/mt, down 1.14%. Trading volume reached 15,000 lots, and open interest stood at 303,000 lots. Overnight, the most-traded SHFE copper 2504 contract opened at 78,140 yuan/mt, initially reaching a high of 78,320 yuan/mt, then fluctuating downward to a low of 78,010 yuan/mt during the session. After a slight rebound, it pulled back again and finally closed at 78,070 yuan/mt, down 0.47%. Trading volume reached 19,000 lots, and open interest stood at 164,000 lots.

【SMM Copper Morning Brief】News: (1) US Secretary of Energy stated that President Trump might lift tariffs on Canadian oil in April.

(2) The latest consumer expectations survey by the New York Fed showed that US short-term inflation expectations rose in February, while medium and long-term inflation expectations remained stable. Public expectations for financial conditions worsening over the next year were the strongest since November 2023.

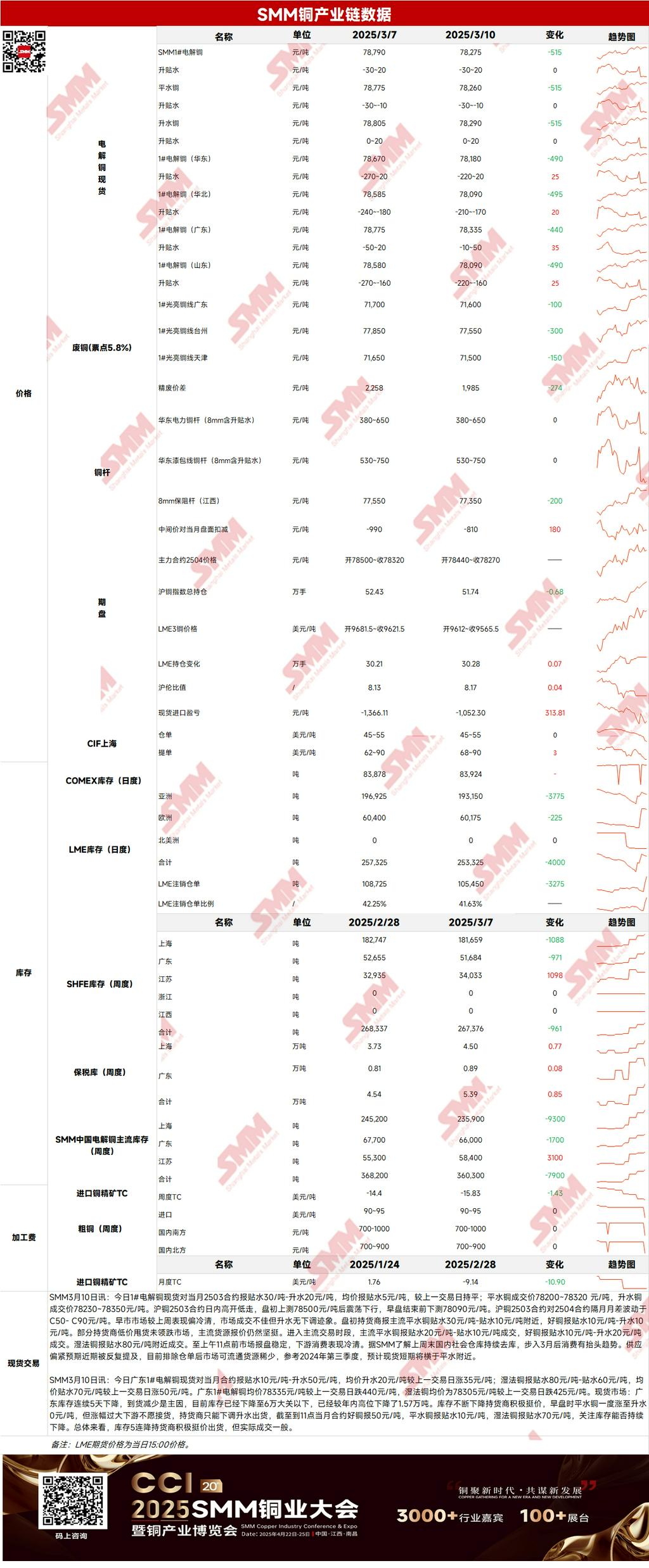

Spot Market: (1) Shanghai: On March 10, #1 copper cathode spot prices against the front-month 2503 contract were quoted at a discount of 30 yuan/mt to a premium of 20 yuan/mt, with an average price at a discount of 5 yuan/mt, flat WoW. According to SMM, domestic social warehouses continued destocking over the weekend, and consumption showed signs of improvement in March. Tight supply expectations have been repeatedly mentioned recently, and excluding warehouse warrants, marketable supply remains scarce. Referring to Q3 2024, spot prices are expected to hover near parity in the short term.

(2) Guangdong: On March 10, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 10 yuan/mt to a premium of 50 yuan/mt, with an average premium of 20 yuan/mt, up 35 yuan/mt WoW. Overall, inventories have declined for five consecutive weeks, and suppliers actively stood firm on quotes, but actual transactions were moderate.

(3) Imported Copper: On March 10, warehouse warrant prices were $45-55/mt, QP March, with the average price flat WoW; B/L prices were $68-90/mt, QP April, with the average price up $3/mt WoW. EQ copper (CIF B/L) was quoted at $10-20/mt, QP March, with the average price up $1/mt WoW. Quotes referenced cargoes arriving in mid-to-late March and early April. Yesterday, the SHFE/LME price ratio for the SHFE copper 2503 contract was around -1,100 yuan/mt. LME copper 3M-Mar was at B$5.9/mt, LME copper 3M-Apr was at B$5.97/mt, and the March date to April date spread was around C$0.07/mt. Suppliers were not very active in quoting yesterday, and market sentiment cooled significantly compared to last Friday. Scattered quotes for domestic warehouse warrants and EQ copper were heard, but transactions were rare.

(4) Secondary Copper: On March 10, secondary copper raw material prices fell by 100 yuan/mt MoM. Guangdong bare bright copper prices were 71,500-71,700 yuan/mt, up 200 yuan/mt WoW. The price difference between primary metal and scrap was 1,985 yuan/mt, down 273 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,325 yuan/mt. According to the SMM survey, copper price pullbacks combined with the price difference between primary and secondary copper rods remaining above the advantageous threshold have led to a recovery in downstream orders. Secondary copper rod enterprises indicated that expectations for the traditional consumption peak season are marginally improving.

(5) Inventory: On March 10, LME copper cathode inventories decreased by 4,000 mt to 253,325 mt. On the same day, SHFE warrant inventories decreased by 893 mt to 156,594 mt.

Prices: Macro side, Trump acknowledged that his comprehensive tariff policy might bring some "short-term" pain to Americans and did not rule out the possibility that tariff-related pain could lead to a recession. This statement heightened market risk aversion, causing the US dollar index to rebound, which pressured copper prices. Additionally, concerns that US tariff policies might drag down the global economy and weaken energy demand led international oil prices to fall to a six-month low, further weighing on copper prices. Fundamentals side, high copper prices have suppressed domestic downstream consumption. However, with the consumption peak season approaching, copper price pullbacks are expected to boost downstream orders. As of March 10, SMM data showed that copper inventories in major regions nationwide decreased by 8,000 mt WoW to 360,000 mt. Notably, current domestic inventories are already below the levels of the same period last year, indicating a turning point in inventory trends. Looking ahead to this week, the opening of the export window is expected to drive increased exports and reduced imports. Combined with a recovery in consumption during the production peak season, social inventories are expected to continue declining. In terms of prices, copper prices are expected to maintain a stable fluctuating trend today.

》Click to View the SMM Metal Database

【The above information is based on market data collected and comprehensive evaluations by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】